China’s R&D super deduction policy allows eligible companies to deduct double of their qualifying R&D expenses from taxable income, fostering innovation and reducing corporate income tax obligations.

Background

Initially launched in 2008, the policy has evolved to relax definitions and extend benefits to wider enterprise categories. In 2023, the super deduction rate was officially extended indefinitely to 200% for most companies. Prior to that, some specialized enterprises, including qualified small and medium-sized technology enterprises, could enjoy slightly different deduction percentages (e.g., 175%, 150%)

Deduction rate

Eligible enterprises can deduct 200% of their actual R&D expenses that do not result in intangible assets, meaning they get to deduct the expenses twice — the actual cost (100%) plus an additional 100% super deduction. For R&D expenses that do create intangible assets (e.g., patents), amortization can be deducted at 200% of the cost with no time limit on amortization.

- Non-intangible asset R&D expenses: Deductible at 200% (actual cost plus an equal super deduction).

- Intangible asset related R&D expenses: Amortized at 200% of the cost over the useful life without a time limit.

- Related expenses (supporting R&D): Limited to a maximum of 10% of the total deductible R&D expenses.

Scope

The policy covers all resident enterprises that meet accounting and compliance standards, excluding industries on the national “negative list”, such as real estate, financial services, and some entertainment sectors. Beneficiary sectors include advanced manufacturing, IT, new energy, and environmental technologies.

Applicants must be involved in systematic activities aimed at acquiring new scientific or technological knowledge, or substantially improving products, services, or processes, excluding routine testing or quality control. Enterprises must keep clear, detailed records on their R&D projects, including project descriptions, objectives, expenditures, personnel involved, outcomes, and evidence to present to tax authority audits.

Examples of eligible R&D activities for China’s R&D super deduction typically include:

- Development and improvement of new or existing products, services, or processes involving scientific or technological innovation beyond routine upgrades or quality control.

- Designing, manufacturing, and testing of prototypes and pilot models.

- Systematic research projects aimed at overcoming technological problems or achieving specific technical breakthroughs.

- Activities that seek to enhance technological performance, such as improving response speeds in automotive brake systems or developing advanced manufacturing automation.

- Experimental development to acquire new scientific knowledge or substantially improve existing technology.

- Supporting activities directly related to R&D, such as expert consulting, technological assessments, product testing, evaluation, and acceptance procedures.

- Costs related to patent applications, IP rights protection, and associated technology-related services may qualify as related expenses (capped at 10% of total R&D expenses).

Application

Companies apply for the super deduction during regular tax filings when filing quarterly, semi-annual, or annual corporate income tax returns. For example, the super deduction for R&D expenses incurred in the first half of the year must be applied during the July filing period.

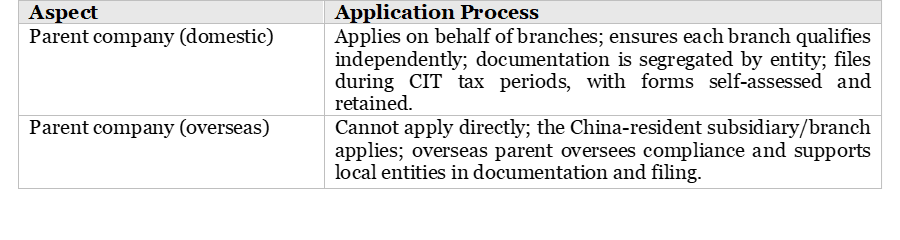

For the parent company application process regarding China’s R&D super deduction:

- When a parent company applies on behalf of its branches or subsidiaries, it must ensure that each entity independently meets the eligibility criteria for super deduction. The parent company typically consolidates or coordinates the application process but should maintain clear, distinct documentation reflecting the R&D activities and expenses of each branch or subsidiary.

- The responsible entity (parent company or a specific branch) applies for the super deduction during the corporate income tax filing periods—quarterly, semi-annually, or annually. For example, R&D expenses incurred in the first half of 2025 are applied for in the July 2025 tax filing.

- The application is self-assessed with the taxpayer calculating the eligible expense amount and filling in the relevant tax forms, such as the “CIT Monthly (Quarterly) Prepayment Return (Class A) Form” and the “R&D Expense Super Deduction Details Form (A107012).” This documentation must be preserved for potential tax authority reviews or audits.

The parent company is an overseas (foreign) company:

- The super deduction policy generally applies to resident enterprises in China. If the parent company is overseas, the application responsibility lies with the China-resident subsidiary or branch conducting the R&D activities, as only Chinese resident enterprises qualify directly for the deduction.

- The overseas parent company itself does not directly apply for the super deduction but can coordinate or guide the qualified China-based entities under its group to properly document and claim the deductions.

- The China tax authorities require that entities claiming the deduction have proper accounting and compliance status under Chinese law. Overseas parents must ensure their Chinese affiliates fulfill these requirements.

This arrangement ensures that the China-based entity performing R&D and incurring expenses receives the tax benefit while the overseas parent supports compliance across the group.

Invest in China Safely

As global economic dynamics evolve and regulatory frameworks shift, navigating China’s investment landscape requires both precision and foresight. The latest tax credit policy for foreign-invested enterprises signals China’s strategic intent to retain foreign capital while fostering long-term growth. For businesses weighing the risks and rewards of reinvestment, expert guidance is key. Reach out to our experts at contact@sjgrand.cn for a China strategy custom-made for your industry and business needs.

Latest Articles: