Hong Kong’s offshore tax exemption regime is one of the key features that strengthens its competitiveness and appeal to international businesses. Under this framework, profits that are sourced outside Hong Kong are exempt from local taxation—effectively applying a 0% tax rate to qualifying offshore income. Eligible offshore income may include service fees, passive income derived from the offshore use of intellectual property, and disposal gains that satisfy the conditions for intra-group relief.

To successfully substantiate an offshore (foreign-sourced profits) claim, businesses must provide a clear and consistent paper trail. This documentation should demonstrate that the core profit‑generating activities—such as decision-making, management, and operational processes—were carried out outside Hong Kong, rather than relying solely on the fact that customers or counterparties are located overseas.

Core principle

Hong Kong adopts a territorial system of taxation, under which only profits arising in or derived from Hong Kong are subject to Profits Tax. Accordingly, it is the taxpayer’s responsibility to prove that the relevant profits were derived from activities undertaken outside Hong Kong.

To justify an offshore (foreign‑sourced profits) claim, businesses must maintain a clear and consistent paper trail. This documentation should demonstrate that the profit‑generating activities—such as key management functions, decision‑making, and operational processes—took place outside Hong Kong. Simply having customers or transaction counterparties located overseas is not sufficient on its own to support an offshore claim.

Key evidence categories

Businesses typically need to prepare evidence across four main areas to justify an offshore claim:

- Operational workflow: where contracts and business are carried out

Evidence should show that the core activities leading to the profit generation occur outside Hong Kong:

- Contracts and agreements with non–Hong Kong customers or suppliers, demonstrating that negotiation, signing, and execution took place outside Hong Kong.

- Invoices, purchase orders, and transaction records consistent with overseas counterparties and offshore performance locations.

- Emails and other communication records indicating that negotiations, instructions, and decision‑making were handled outside Hong Kong.

- For businesses where sales and service delivery occur primarily online, supporting documentation will be required to prove that the income is foreign‑sourced. This includes the names of the platform(s) used to deliver services, relevant website links, and evidence showing where activities were performed.

- Documentation of after‑sales support workflows and the location of personnel.

- Management and control outside Hong Kong

To demonstrate that central management and control are exercised outside Hong Kong, a business must show that the “real business mind” — where strategic decisions are made and implemented — is situated offshore. Merely having overseas directors is not sufficient if Hong Kong based staff negotiate contracts and management only signs off.

- Board minutes and resolutions confirming that meetings and key decisions were made outside Hong Kong.

- Travel records, itineraries, and expense claims show that senior personnel conducted negotiations and management activities while overseas.

- Organizational charts and employment contracts demonstrating that operational and managerial staff are based outside Hong Kong.

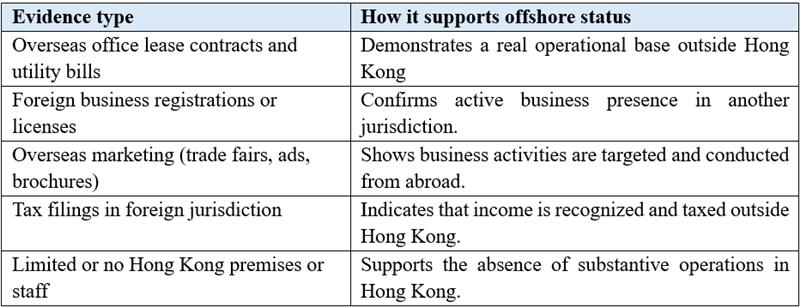

- Operational substance abroad and lack of local operations

Providing evidence of genuine offshore operations—and minimal substantive activity in Hong Kong—strengthens an offshore claim.

- Accounting and banking trail

Financial records must clearly differentiate offshore income from Hong Kong sourced activities:

- Separate profit‑and‑loss accounts for Hong Kong and offshore activities, with transparent allocation of shared costs.

- Accounting ledgers that distinctly track foreign‑sourced income and related expenses.

- Bank statements showing receipts from and payments to overseas parties, ideally through offshore bank accounts connected to foreign operations.

- Foreign currency transaction records evidencing genuine cross‑border dealings.

- Documentation showing the place where sales invoices were issued.

Sector‑specific evidence examples

- Trading of goods: Bills of lading, airway bills, customs documents, and warehouse receipts confirming goods move directly between non‑Hong‑Kong locations and do not pass through Hong Kong.

- Services: Records of where services were actually performed (timesheets, travel records, service reports, logs of remote work from overseas).

- E‑commerce and digital: Server locations, website analytics showing customer locations, and records of platform operations managed outside Hong Kong.

- IP/royalties: Licensing agreements, foreign IP registrations, and royalty statements showing exploitation and management of IP in other jurisdictions.

Common Reasons for Rejection

Hong Kong’s Inland Revenue Department (IRD) tends to reject offshore (foreign‑sourced profits) claims when the facts or documents do not convincingly show that profits were generated outside Hong Kong, or when they suspect tax‑avoidance motives.

- Lack of documentary evidence

The most common reason is insufficient, inconsistent, or missing documentation to prove where core profit‑generating activities actually took place (contracts, correspondence, logistics, banking trail, etc.).

- Focus only on contract signing location

Companies often rely solely on the place where contracts are signed, but the IRD looks at the whole value chain (negotiation, decision‑making, logistics, financing, risk management) and may conclude part of the business was in Hong Kong.

- Hidden or underestimated Hong Kong activities

Using Hong Kong staff, premises, trade finance, shipping arrangements, or management functions, while claiming the profits are offshore, leads the IRD to treat those Hong Kong activities as core operations and deny the claim.

- No real substance in the claimed “offshore” structure

Where the Hong Kong company bears little risk, has no staff, yet keeps high margins, or relies entirely on related overseas parties without proper cost recharges or agency arrangements, the IRD may regard the setup as artificial and tax‑driven.

- Profits not taxed anywhere (double non‑taxation)

If the same profits are not taxed in any other jurisdiction, the IRD is increasingly reluctant to grant offshore status and may infer that the activities were effectively carried out in Hong Kong.

- Poor, late, or inconsistent responses to IRD enquiries

Vague explanations, contradictions between documents and narratives, or failure to provide requested information within deadlines can undermine credibility and result in rejection.

What happens after rejection

The IRD treats the profits as Hong Kong‑sourced and raises/adjusts assessments, including potential interest on underpaid tax.

The taxpayer can object and, if necessary, appeal to the Board of Review or the courts, but success depends on producing strong, consistent evidence of offshore sourcing.

Practical tips

We handled cases when the offshore status claim was not reviewed for a decade until the IRS challenged Hong Kong offshore status and requested tens of thousands in back taxes. To avoid fines and back taxes in the future, we strongly recommend storing all the records.

- Maintain contemporaneous documentation (not recreated later), organized by deal, client, and jurisdiction.

- Ensuring consistency: contracts, emails, travel, and bank records should tell the same story about where the profits are generated.

- Prepare a concise written explanation (e.g., operational flow chart or narrative) linking all documents to show how profits are derived offshore.

- Expect detailed questions from the Inland Revenue Department (IRD) and keep records for at least the statutory retention period.

Looking for case-specific support?

If your business was refused an offshore status and you require assistance reviewing the eligibility of the company for offshore status and structuring your offshore claim file or ensuring compliance with Hong Kong tax law while minimizing financial exposure – we are here to assist. We provide customized reviews of your company’s tax compliance status and identify potential risks. From tax planning strategies to regulatory compliance consulting and process optimization, our experts help you minimize risks, avoid penalties, and maintain a strong compliance posture.

Partner with us for expert tax advisory and compliance support. Contact us today to schedule your corporate health check and build a customized compliance roadmap for 2026.

Latest Articles: